AI in Property Valuation: The Complete Guide to Smarter, Data-Driven Pricing Models

The Revolution Quietly Transforming Real Estate-The Moment Everything Started Changing

In 2018, something subtle but profound began shifting in the real estate industry. Not with a headline or announcement, but quietly, through adoption numbers that few people noticed at first.

Zillow, the online real estate platform, announced that its automated valuation model—the Zestimate—had been accessed by more than 200 million users in a single month. At the same time, mortgage lenders began replacing human appraisers with algorithms for initial property screening. Investment firms started using machine learning to identify undervalued properties before human scouts could. Real estate technology companies raised billions in venture capital specifically to build AI-powered valuation platforms.

The revolution wasn’t dramatic. There were no riots against the machines. No news headlines proclaimed “AI Destroys Real Estate Industry.” Instead, the change happened gradually, through thousands of small decisions by lenders, investors, platforms, and professionals who quietly recognized that AI could do something humans couldn’t: process enormous amounts of data, spot subtle patterns, and generate consistent valuations faster and often more accurately than traditional methods.

Today, in 2025, we’re at an inflection point. AI isn’t replacing property valuation—it’s fundamentally transforming how valuations happen. And if you work in real estate, invest in property, or are buying or selling, this shift matters to you.

Why This Matters Right Now

The real estate market is enormous. According to the World Economic Forum, global real estate transactions exceed $7 trillion annually. Even small percentage improvements in valuation accuracy, speed, or consistency represent hundreds of billions of dollars in better decision-making.

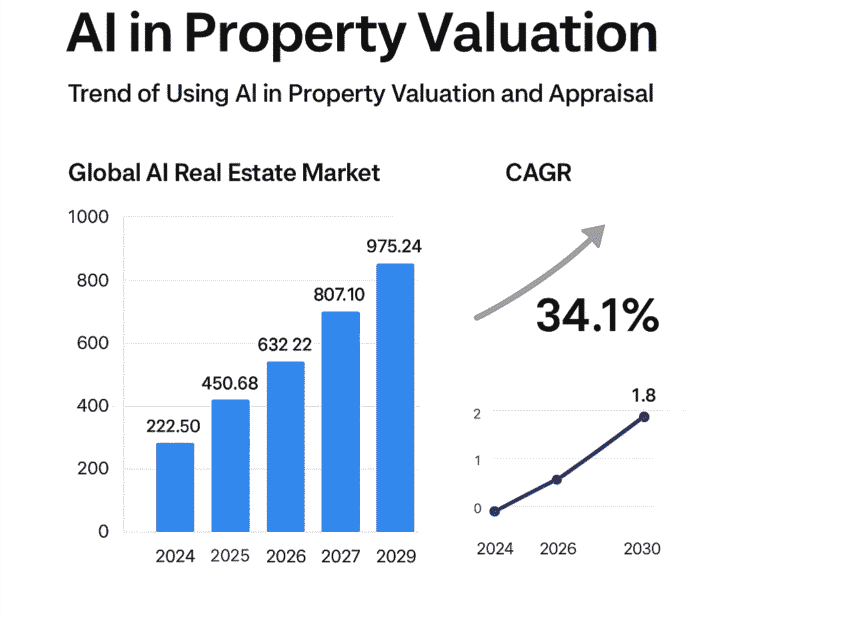

According to Research and Markets, the AI in the real estate market is growing at a 35% CAGR and is expected to reach a value of $975–978 billion by 2029. Source-

But the opportunity isn’t just about scale. It’s about accuracy and fairness. Traditional property appraisals have long carried a problem that nobody really talked about openly: inconsistency. Two appraisers could value the same property differently. Geography, appraiser experience, personal biases, and subjective judgment all influenced the outcome.

A property that one appraiser valued at $450,000 might be valued at $485,000 by another, simply because they were different people with different perspectives.

AI doesn’t solve all bias, but it does something important: it makes bias detectable and correctable. When valuation errors occur in algorithmic systems, you can trace them to specific data inputs or model assumptions. You can’t do that with human judgment.

Additionally, the speed advantage is genuinely transformative. In competitive real estate markets, speed is money. Every day a property sits unvalued is a day a competitive offer goes elsewhere. By cutting valuation time from weeks to days or hours, AI creates genuine economic value.

Suggested Reading: How AI is Transforming Real Estate: Use Cases, Benefits, and Future Trends

What You’ll Learn in This Guide

This comprehensive guide takes you on a journey from “what is property valuation?” to “how does AI change everything?” We’ll cover:

- How traditional appraisals work and why they have limitations

- The specific technologies and methodologies AI uses for valuation

- Who’s implementing these systems and with what results

- The genuine limitations and ethical considerations

- How different stakeholders—buyers, sellers, lenders, investors, professionals—will experience this change

- What the future actually looks like (not the hype version)

- How you can prepare for and benefit from these changes

By the end, you’ll understand not just what AI is doing to property valuation, but why it matters and how to position yourself or your organization to lead rather than follow this transformation.

Understanding Traditional Property Valuation

The Historical Context: Why Appraisals Became the Standard

Property valuation isn’t new. People have been estimating property values for centuries—at least since real estate became something you could buy and sell separately from the land you farmed on it.

For most of modern history, property valuation was entirely subjective. An estate agent would visit a property, develop an intuitive sense of its value based on their experience, and suggest a price. Buyers and sellers would negotiate from there. There was no systematic method, no data analysis, just professional judgment and negotiation skill.

This changed in the early 20th century, especially after real estate markets became critical to banking and lending. Banks needed consistent ways to determine whether a $200,000 property was actually worth $200,000 before they’d lend money on it. If a bank lent $150,000 on a property they later discovered was only worth $120,000, and the borrower defaulted, they’d lose money. They needed better systems.

Enter the appraisal profession. Formal property appraisal emerged in the United States during the 1930s, following bank failures during the Great Depression. If banks had had better valuation methods, the logic went, they might have avoided lending on overvalued properties. Professional appraisers were trained in systematic methods. They developed the “Comparative Market Analysis” (CMA) approach, which became the backbone of American real estate valuation.

The CMA methodology, which remains the standard today, works like this: an appraiser identifies recently sold properties similar to the subject property (comparables, or “comps”). They analyze the prices of these comparable properties, adjusting for differences in features, location, and condition. From this analysis, they estimate the value of the subject property. It’s logical, systematic, and represents a huge improvement over pure intuition.

How Traditional Appraisals Work Today

Let’s walk through an actual appraisal process as it happens in 2025:

Step 1: Commission and Initial Review

A lender, buyer, or seller commissions an appraisal. The appraiser receives the property address and some basic information. They might spend 15-30 minutes reviewing available public data: property tax records, previous sales history, MLS listings, and neighborhood information.

Step 2: The Physical Inspection

The appraiser schedules a visit to the property. This is crucial—they can’t appraise a property they haven’t seen. During the inspection, which typically lasts 30-90 minutes for a residential property, they:

- Measure the square footage (many appraisers still do this manually with a measuring wheel)

- Count rooms and assess their condition

- Evaluate the roof, foundation, siding, and exterior

- Note upgrades or defects

- Take photographs

- Document any issues affecting value

- Assess neighborhood characteristics

For a $400,000 home, this might be the only person to physically evaluate it before the sale closes.

Step 3: Comparable Selection

The appraiser then identifies comparable properties. “Comparable” means recently sold properties that are similar to the subject property in terms of location, size, type, age, and condition. For a suburban home, this might mean looking at 3-6 sales that occurred in the last 3-6 months within a mile or so.

The challenge here is immediate: there might not be perfect comparables. Maybe your house is a unique Victorian on a tree-lined street. The “comparables” might be newer ranch homes on busier roads. The appraiser adjusts for these differences, but the adjustments are subjective.

Step 4: Adjustment and Analysis

For each comparable, the appraiser notes differences from the subject property and makes adjustments. If a comparable is 500 square feet smaller, the appraiser might add value. If it has a newer roof, they might subtract. These adjustments vary by appraiser. There’s no precise science for “how much is a new roof worth?”—it depends on the market, the age of the subject property’s roof, and the appraiser’s judgment.

Step 5: Report and Final Opinion

The appraiser synthesizes their findings into a formal report, typically 15-30 pages. This report includes:

- Property description and photographs

- Neighborhood analysis

- List of comparable properties with adjustments

- The appraiser’s final value estimate

- Limiting conditions and assumptions

The entire process, from initial review to final report, typically takes 5-10 business days. Lenders rely on these reports to make lending decisions worth hundreds of thousands of dollars.

The Strengths of Traditional Appraisal

Before we discuss limitations, let’s acknowledge what traditional appraisals do well:

Comprehensive Local Knowledge: An experienced appraiser who’s been working in a market for 20 years understands things no algorithm has seen yet. They know that a property on a quiet street versus a busy street differs in value by 8-12%, not the 2% the algorithm calculated. They remember the last housing crash and what preceded it. They understand local development plans and economic currents.

Edge Case Handling: Unusual properties—historic homes, multi-use buildings, properties with quirks—are genuinely difficult for algorithms. An experienced appraiser can incorporate judgment, context, and nuance that data alone can’t capture.

Relationship Trust: Appraisers build reputations. They work repeatedly with the same lenders and real estate professionals. There’s professional accountability. If an appraisal is wildly off, it affects the appraiser’s career. This creates an incentive for accuracy.

Legal Recognition: Traditional appraisals have been accepted in courts, by regulators, and in official documents for decades. They carry legal weight. When a property needs to be valued for tax purposes, estate settlement, or litigation, courts generally accept appraisal reports.

Contextual Adjustment: Appraisers can incorporate information that hasn’t yet been reflected in data. A new highway is coming soon, which affects value. A major employer is leaving town—that matters. A neighborhood is in the early stages of gentrification—that changes things. An appraiser can factor these forward-looking considerations into their analysis in ways historical data can’t.

These are genuine strengths. Understanding them helps explain why traditional appraisals haven’t disappeared—and won’t, even with AI advancement.

The Time and Cost Reality

Despite their strengths, traditional appraisals have a significant practical problem: they’re slow and expensive.

A typical residential appraisal costs $300-500. For commercial properties, the cost might be $1,000-5,000 or more. For a lender processing thousands of applications, this represents significant cost. For a buyer who wants a valuation before making an offer, the 5-10 day timeline is often too slow.

From a capital efficiency perspective, traditional appraisals represent a bottleneck. You want to close on a property in 30 days. But if valuation takes 10 days, inspection takes 2 days, underwriting takes 5 days, and final approval takes 3 days, you’ve barely made it. Any delay cascades through the whole process.

Additionally, consistency is expensive. Two appraisers will sometimes produce very different valuations on the same property. This creates disputes, requiring additional appraisals, further delays, and additional costs.

The Regulatory Context

It’s important to understand that property appraisals aren’t just professional practice—they’re heavily regulated. In the United States, appraisers must be licensed. They must follow the Uniform Standards of Professional Appraisal Practice (USPAP). They must comply with various federal regulations including the Dodd-Frank Act and the Home Valuation Code of Conduct.

These regulations exist for good reasons—to protect consumers and maintain the integrity of the lending system. But they also create barriers to change. You can’t just replace appraisers with algorithms overnight without changing regulations, and regulations change slowly.

This regulatory context is important for understanding why AI adoption in valuation has been gradual and why it remains hybrid—algorithms assist or augment human judgment rather than completely replacing it.

The Limitations of Human-Only Appraisals

Bias and Inconsistency: The Elephant in the Room

Here’s a truth that the real estate industry has grappled with for decades, though it’s rarely discussed openly: professional appraisers are not perfectly objective.

Research has documented this extensively. Studies have found that factors like the appraiser’s own race or neighborhood familiarity can influence their valuations. Properties in certain neighborhoods are sometimes appraised lower than comparable properties elsewhere, even after accounting for objective factors.

The phenomenon is sometimes called “appraisal bias” or “neighborhood bias,” and it has real consequences.

In 2020, this issue received major attention when various lawsuits and investigations revealed that homes owned by Black families were being systematically undervalued.

Example of Bias in Traditional Appraisals

Tenisha Tate-Austin and her husband became suspicious when their Northern California home—one they had spent years renovating—was appraised far below their expectations.

Seeking clarity, they requested a second appraisal. This time, a White friend posed as the homeowner, and the couple removed family photos and artwork that reflected their identity.

The result was staggering: the new appraisal for their Marin County property came back at more than $1.4 million, nearly half a million dollars higher than the previous estimate.

The case drew national attention and underscored how racial bias can influence human-driven property valuations—a challenge that data-driven AI systems are now being designed to minimize through standardized, transparent modeling.

These aren’t isolated incidents. Federal Reserve research, studies by nonprofit advocacy groups, and litigation have all documented systematic disparities. The cause is complex—some bias is conscious, some unconscious.

Some reflect genuine economic factors (properties in neighborhoods with lower incomes do often have more limited appreciation potential), but some reflect prejudice and historical discrimination that shouldn’t influence valuations.

The Subjectivity Problem

Even well-intentioned appraisers make subjective judgments that vary from person to person:

Comparable Selection: How many comparables do you look at? How wide a geographic radius? How far back in time? Two appraisers can make different choices here, which affects the final valuation. If you’re looking at a property that sold 6 months ago versus 8 months ago, which is more relevant? It depends on whether the market is appreciating or depreciating—and how much.

Adjustment Amounts: When adjusting for differences between the subject property and comparables, how much is a new roof worth? $3,000? $8,000? It depends on the property value, the local market, and the appraiser’s judgment. A $50,000 adjustment difference isn’t unusual for high-value properties, and that’s purely from judgment calls.

Condition Assessment: Is the foundation “good” or “fair”? Is the kitchen “updated” or “adequately maintained”? These descriptions are subjective, and they influence value. Different appraisers might rate the same property differently.

Neighborhood Assessment: One appraiser might see a neighborhood as “transitional with potential.” Another might see it as “declining.” Both might be looking at the same data but interpreting its significance differently.

When you compound these subjective judgments, you get significant variance in appraisals. Studies have documented that getting two appraisals on the same property can result in 5-15% differences, sometimes more. For a $400,000 property, that’s a $20,000-60,000 range from subjectivity alone.

The Information Problem

Here’s something that often surprises people: traditional appraisals don’t actually incorporate that much data. An appraiser might look at 3-6 comparable sales, neighborhood crime statistics, school ratings, and maybe some economic data. That’s it. It’s a fraction of the information available.

Consider all the data that could be relevant to a property’s value but that a traditional appraisal might not systematically incorporate:

- Proximity to amenities (coffee shops, restaurants, parks, grocery stores)

- Walkability scores and transit accessibility

- Historical crime trends (not just current statistics)

- Air quality and environmental factors

- Traffic patterns and noise levels

- School performance trends over time (not just current ratings)

- Neighborhood gentrification potential

- Demographic shifts

- Employment center proximity

- Property tax trends

- Insurance costs

- Utility expenses

- Historic preservation restrictions

- Natural disaster risk

- Microclimate differences between neighborhoods

An experienced appraiser might have an intuitive understanding of some of these factors, but they don’t systematically incorporate all of them. A comprehensive algorithm can.

The Time Lag Problem

Property valuations are point-in-time estimates. By the time an appraisal report is completed, it’s already a week old. If market conditions are changing rapidly (which they are in many markets), the valuation is stale before it’s even used.

This became especially apparent during the pandemic and the subsequent boom and correction in real estate. Properties that sold for $400,000 in May could sell for $425,000 in June and $415,000 in August. A traditional appraisal from July was immediately partially out of date.

AI systems, by contrast, can update continuously. As new sales data enters the system, valuations adjust automatically. This creates fundamentally different information in real-time markets.

The Geographic Limitation

Traditional appraisals scale by appraiser availability. In some markets, there are hundreds of qualified appraisers. In others, there are dozens. This creates bottlenecks and can make appraisals slow in less-developed markets or during busy seasons.

An AI system scales infinitely—it can value a property just as easily in rural Montana as in Manhattan (though accuracy might vary based on data availability).

The False Confidence Problem

Here’s a subtle but important issue: traditional appraisals present themselves with more confidence than is justified.

An appraiser concludes that a property is worth exactly $487,500. That number is presented as fact in a formal report. But the truth is much less certain. The appraiser’s analysis probably has a margin of error of ±5-10%, sometimes more. Yet the report format—and the legal weight appraisals carry—makes it seem like $487,500 is the definitive correct number, not a best estimate with significant uncertainty.

AI systems, increasingly, present valuations with confidence intervals: “This property is likely worth $475,000, with a 68% confidence that it falls between $450,000 and $500,000.” This is more honest about uncertainty.

The Cost-Benefit Tradeoff

For a $50,000 property in a rural area, a $400 appraisal fee represents 0.8% of the property value. For a $5,000,000 property, it represents 0.008%. The smaller properties are getting relatively expensive valuations, yet the valuations are based on potentially fewer comparable sales and more sparse data.

This creates a market opportunity: AI can provide useful valuations at much lower cost for smaller properties or less-developed markets, while traditional appraisals remain valuable for high-complexity, high-value properties.

What Is AI-Powered Property Valuation?

The Basic Concept

Let’s start with something fundamental: what exactly is artificial intelligence in the context of property valuation?

In the broadest sense, AI (in this context) means machine learning algorithms that learn patterns from historical data and apply those patterns to new situations. It’s not a sentient computer making human-like decisions. It’s software that identifies statistical relationships in data.

Here’s a simple example. Imagine you had data on 10,000 houses that sold in a market over the past five years. For each house, you know:

- Price

- Square footage

- Number of bedrooms

- Number of bathrooms

- Lot size

- Age of the building

- Condition

- Proximity to transit

- Proximity to schools

- Neighborhood

A machine learning algorithm would look at all this data and identify patterns. It might learn:

“Houses close to good schools sell for about 8% more than otherwise identical houses far from schools.”

“Every additional bedroom adds about $45,000 to house value.”

“For every mile further from downtown, price drops about 3% per mile, but only up to 5 miles; beyond that, the drop per mile decreases.”

“Newer houses sell for more than older ones, but the depreciation slows over time.”

These patterns aren’t programmed in—they’re discovered by the algorithm analyzing the data.

Once the algorithm learns these patterns from historical data, you can apply it to a new house: give it the square footage, bedroom count, school proximity, and other features, and it will predict what the house should be worth based on the patterns it learned.

That’s the core of AI property valuation.

The Types of AI Systems in Use

When people talk about “AI property valuation,” they’re usually referring to one of three approaches:

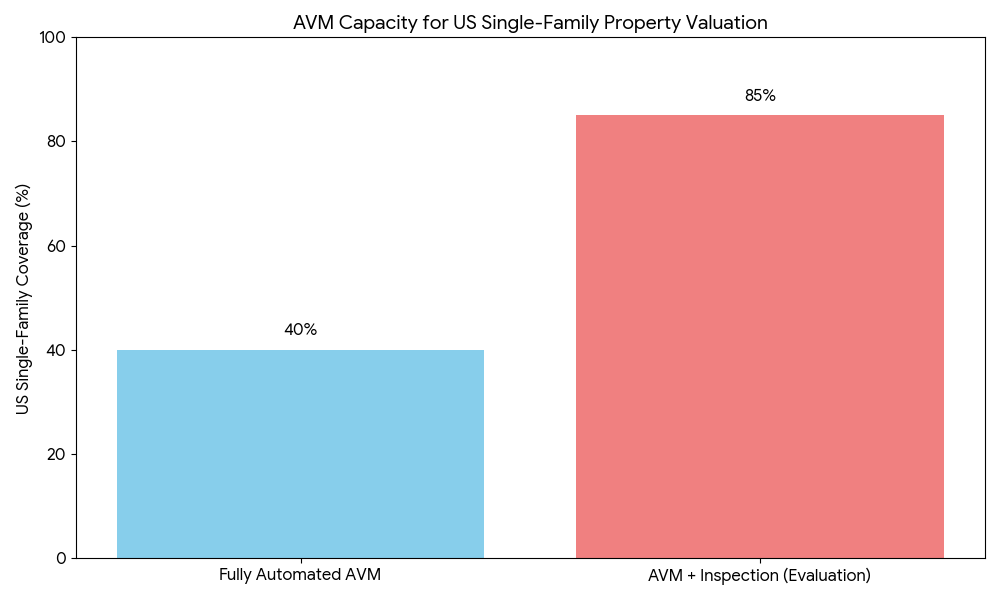

Automated Valuation Models (AVMs): These are pure algorithmic systems with minimal human involvement. You input property data, and the algorithm outputs a valuation. Zillow’s Zestimate, Redfin’s Estimate, and CBRE’s CORE valuation tool are examples. AVMs are fast (seconds), cheap (often free or very low cost), and scale infinitely. But they have limitations in edge cases and unique properties.

Below Image- AVM & AVM+Human property valuation model adoption across US.

Hybrid Appraisal Systems: These combine algorithmic valuation with human review. An AI system generates an initial valuation and flags it as “high confidence,” “medium confidence,” or “low confidence” based on data availability and comparability. A human appraiser then reviews cases flagged as low confidence. This approach balances speed and accuracy. Lenders increasingly use this method.

AI-Assisted Appraisal: This is where an appraiser uses AI tools to enhance their work—automated comparable finding, automated adjustments, data visualization—but the appraiser remains in control. It’s not replacing the appraiser; it’s making them more efficient. Many professional appraisers are moving toward this model.

Each approach serves different purposes and different market segments.

The Data Requirements

AI valuation systems are only as good as the data they’re trained on. To build an effective AI valuation model, you need:

Historical Transaction Data: Sale prices, dates, and terms for thousands (ideally tens of thousands or millions) of properties. This includes not just price but the conditions of the sale—was it an arms-length transaction or a family transfer? Was it in foreclosure? This matters because a foreclosure sale price is usually lower than a fair market transaction.

Property Characteristics Data: Details about each property—square footage, lot size, year built, number of bedrooms, condition, recent renovations, etc. This data comes from property tax records, MLS listings, county assessor databases, and sometimes photos/satellite imagery.

Locational Data: Geographic information about neighborhoods—school ratings, crime statistics, walkability scores, transit proximity, median household income, employment centers, etc.

Temporal Data: How values have changed over time, allowing the algorithm to account for appreciation or depreciation trends.

Transactional Context: Information about the market conditions at the time of each sale—was the market appreciating or depreciating? What were interest rates? This helps the algorithm understand market-wide factors versus property-specific factors.

The companies and platforms that have the most effective AI valuation systems are those with the most data. Zillow, Redfin, and national lenders have access to massive datasets—millions of historical transactions, property photos, neighborhood data, and more. They’re constantly updating their systems with new data, which improves accuracy.

The Technology Stack

Behind the scenes, AI property valuation systems typically use:

Data Collection and Preparation: Before algorithms can learn patterns, data needs to be collected, cleaned, and standardized. Property features recorded differently in different databases need to be harmonized. Outliers and errors need to be identified. This is sometimes 80% of the work—the boring infrastructure that makes the sexy algorithms possible.

Machine Learning Algorithms: Multiple types are often used in ensemble (combined) models:

- Random Forests: These work by building many decision trees and averaging their predictions. They’re robust and good at handling non-linear relationships.

- Gradient Boosting: These iteratively build predictive models, each correcting errors from the previous one. XGBoost and LightGBM are popular implementations.

- Neural Networks: Deep learning approaches that can capture complex, non-linear patterns in data. They require more data and computational power but can sometimes achieve higher accuracy.

- Support Vector Machines: Algorithms that find optimal boundaries between different classes or values. Good for classification and regression problems.

Most sophisticated systems use ensemble approaches—combining multiple algorithms and taking weighted averages of their predictions. No single algorithm is best for all situations.

Feature Engineering: Variables fed into algorithms matter enormously. Raw data often isn’t useful. Engineers create derived features—for example, not just distance-to-school, but also school-quality-weighted distance, where schools are weighted by their quality rating. Good feature engineering can improve model performance dramatically.

Model Validation and Testing: Before deploying a model, it’s tested extensively. Typical approaches:

- Holdout Testing: Train the model on 80% of historical data, test on the remaining 20% the model hasn’t seen.

- Cross-Validation: Divide data into multiple folds, train on different combinations, and validate on left-out folds.

- Out-of-Sample Testing: Test on data from different time periods to ensure the model works across market cycles.

- Stress Testing: What happens when you apply the model to edge cases? Very expensive properties? Unusual property types? Rural markets?

Calibration and Adjustment: Raw model outputs are often adjusted. If the model systematically overestimates in expensive areas or underestimates in emerging neighborhoods, these biases are corrected.

Confidence Scoring: The system estimates its own confidence in each prediction. Properties with abundant comparable data get high confidence scores. Properties in thin markets get low confidence scores.

APIs and Integration: Most modern valuation systems expose their valuations through APIs (application programming interfaces) that other systems can connect to. This allows seamless integration into lending platforms, real estate portals, investment analysis tools, etc.

How Modern AI Actually Generates a Valuation

Let’s walk through a concrete example of how an AI system values a property today:

Input Data:

- Address: 425 Maple Street, Boulder, Colorado

- Square footage: 2,200 sq ft

- Lot size: 0.35 acres

- Built: 1998

- Bedrooms: 4

- Bathrooms: 2.5

- Condition: Good

- Recent renovations: Kitchen remodeled in 2022, Roof replaced in 2019

- Pool: Yes

- Garage: 2-car attached

The Algorithm’s Analysis:

- Data Collection: The system retrieves data on all similar properties that sold in Boulder, nearby suburbs, and the region in the past 12-36 months. It finds 847 comparable transactions.

- Feature Matching: It identifies which properties are actually comparable to the subject property based on square footage, age, bedroom count, etc. It narrows down to 156 reasonably similar properties.

- Neighborhood Contextualization: It pulls in neighborhood data for the subject property’s zip code: median household income ($85,000), crime rate (low), school ratings (high), walkability score (high), proximity to downtown Boulder (2.3 miles), proximity to CU Boulder campus (1.8 miles), median price trend over past 12 months (+4.2%).

- Market Analysis: It checks what the overall Boulder market has been doing—appreciating at about 3-4% annually, with seasonal variation (summer typically stronger than winter).

- Feature Valuation: Using its trained model, it estimates the value contribution of each feature:

- Base price for a 1998 house in Boulder: $380,000

- 2,200 sq ft: adds $110 per sq ft = $242,000

- 4 bedrooms in the Boulder market: adds $25,000

- 2.5 bathrooms: adds $18,000

- Good condition: adds $15,000

- Pool: adds $12,000

- Recent kitchen remodel: adds $8,000

- Recent roof: adds $5,000

- 2-car garage: already factored into base calculation

- Comparable Sales Adjustment: It checks recent comparable sales and notes that similar houses have been selling for 2-5% above what historical patterns suggest. It adjusts upward by 3%.

- Confidence Assessment: It checks data richness. Since Boulder is an active market with good data, it’s highly confident. Confidence score: 92%.

- Final Calculation and Output:

- Computed value: $635,000

- Confidence interval (68% confidence): $615,000-$655,000

- Valuation range with 95% confidence: $595,000-$675,000

- The system outputs: Estimated value: $635,000 with High Confidence

- Explanation: The system generates an explanation: “This property is valued at $635,000 based on 156 comparable properties in the Boulder area. The valuation reflects the property’s size, condition, recent upgrades, and location in a high-demand neighborhood near CU Boulder. The estimated value is 3.2% above the neighborhood median, consistent with the property’s above-average condition.”

This entire process takes seconds. Compare that to a traditional appraisal, which would involve a person visiting the property, spending hours analyzing comparables, and creating a report over 5-10 days.

The Accuracy Question

How accurate are these AI valuations?

Redfin’s AI-powered property valuation model, the Redfin Estimate, claims and delivers high accuracy, to give you one of the most accurate automated home values available. Redfin consistently publishes its precision metrics to ensure transparency.

| Home Status | National Median Error Rate (High Confidence) | What This Means |

| Homes Currently For Sale (On-Market) | $1.93\%$ to $2.1\%$ | For half of all homes listed, the Redfin Estimate is within this small percentage of the final sale price. This is an exceptionally tight margin. |

| Homes Not For Sale (Off-Market) | $7.38\%$ to $7.54\%$ | Even without direct listing details, the estimate remains reliable, with half of the homes falling within this range of their eventual sale price. |

This is important but genuinely nuanced to answer. Accuracy depends on:

Data Availability: In active markets with lots of recent sales and detailed property data (major metropolitan areas, suburbs), AI models often achieve accuracy within ±3-5%. In thin markets (rural areas, specialty properties), accuracy might be ±8-15% or worse.

Property Type: Single-family homes in typical neighborhoods? Good accuracy. Unique properties? Much harder. Commercial properties with varied uses and financing structures? More difficult than residential.

Market Conditions: In stable markets, historical patterns predict well. In rapidly changing markets (gentrification, major economic shift, pandemic effects), historical patterns are less reliable.

Time Horizon: AI is best at “what is this worth today?” It’s less reliable at “what will this be worth in 5 years?”

According to research from Zillow on its own Zestimates, the median error (absolute value) is about 5% for homes they’re able to estimate. Meaning the Zestimate is within 5% of the actual sale price about half the time, and more than 5% off the other half. For properties with more data, accuracy is better. For properties with less data, accuracy is worse.

This is actually pretty good—better than you might expect. It’s comparable to or better than traditional appraisals in many cases, while being dramatically faster and cheaper.

However, “good on average” doesn’t mean “good for every property.” An AI valuation might be within 2% for your neighbor’s house and off by 12% for yours. The confidence scoring helps identify when you should trust the estimate (high confidence) and when you should be skeptical (low confidence).

How Machine Learning Algorithms Value Property

The Mathematical Framework

To truly understand how AI valuations work, you need to understand the basic mathematical framework, though don’t worry—we’ll keep it accessible.

At its core, property valuation is a regression problem: given certain inputs (property characteristics), predict an output (price). Mathematically:

Price = f(square footage, bedrooms, bathrooms, age, location, condition, …) + error

The function f(.) is what the machine learning algorithm learns from historical data. In the simplest case (linear regression), it would be:

Price = w₀ + w₁×square_footage + w₂×bedrooms + w₃×bathrooms + … + error

Where w₁, w₂, w₃, etc. are weights (coefficients) that the algorithm learns. For example, if w₁ = 150, that means the algorithm learned that each additional square foot adds $150 to the price.

The algorithm adjusts these weights by looking at historical data and asking: “What weights minimize the difference between my predictions and actual prices?”

This simple linear model would be something a good statistician could solve with standard regression. But real property valuation is more complex:

Non-Linear Relationships

Property value doesn’t increase linearly with every variable. Consider square footage:

- Going from 1,000 to 1,500 square feet might add $50,000 to value (=$100 per sq ft)

- But going from 3,500 to 4,000 square feet might add only $30,000 (=$60 per sq ft)

Why? Because at smaller square footages, additional space creates proportionally more value. At larger sizes, the marginal value of additional square footage decreases.

This non-linearity applies to many variables. The relationship between age and value is non-linear (very old houses can be valuable). The relationship between distance and value is non-linear (very close to a major highway might be undesirable due to noise and pollution).

Advanced algorithms like neural networks and gradient boosting can capture these non-linear patterns. Linear models would miss them.

Interaction Effects

Variables don’t exist in isolation. Square footage matters more in some neighborhoods than others. Proximity to schools matters more for family-oriented neighborhoods than for urban areas with young professionals.

These interaction effects—where the value of one variable depends on another—are crucial for accurate valuation. Advanced algorithms can capture them.

Overfitting and Regularization

Here’s a subtle but important problem: if you make your algorithm too sophisticated, it can learn the noise in the historical data rather than true underlying patterns.

Imagine you have 1,000 historical properties. If you build a model with 500 parameters (features and interactions), you’ve effectively created a model so flexible that it can fit the noise in the data perfectly. It will predict the 1,000 properties in the training set almost perfectly, but when you apply it to new properties, it will perform poorly. This is called overfitting.

To prevent overfitting, machine learning engineers use regularization techniques—essentially penalizing models that are too complex. The regularized model might be slightly less accurate on the training data but more accurate on new data.

This balance between complexity and generalization is one of the subtle arts of machine learning.

Feature Importance and Interpretability

One advantage of some ML models is that you can determine which features matter most for predictions.

In a property valuation model, you might find that feature importance breaks down as:

- Location factors (proximity to school, walkability, neighborhood safety): 40%

- Physical attributes (square footage, age, bedrooms): 35%

- Condition and upgrades: 15%

- Market timing and trends: 10%

Understanding feature importance helps validate whether the model is learning sensible patterns. If the model said that the color of the front door was the most important factor, you’d know something was wrong.

Training, Validation, and Testing

Building a real machine learning model requires careful separation of data:

Training Set (60-70% of data): The model learns patterns from this data. The algorithm adjusts weights to minimize prediction errors on this set.

Validation Set (15-20% of data): While training, the algorithm periodically checks its performance on validation data it hasn’t trained on. If performance on validation data gets worse while training performance gets better, that signals overfitting. The algorithm stops training before this happens.

Test Set (15-20% of data): After the model is finalized, it’s tested on completely held-out data to get an unbiased estimate of its real-world performance.

This separation is crucial because if you evaluated the model on the same data you trained it on, you’d get unrealistically optimistic performance estimates.

Cross-Validation

Even better than a single train-validation-test split is cross-validation, where:

- Divide all historical data into 5 folds (5 chunks)

- Train on folds 1-4, validate on fold 5

- Train on folds 1-3 and 5, validate on fold 4

- Continue, testing on each fold

- Average the performance across all folds

This uses all the data more efficiently and gives a more robust estimate of performance.

Ensemble Methods

Top-performing valuation models rarely use a single algorithm. Instead, they combine multiple models:

Model 1 (Random Forest): Based on tree-based analysis, learns patterns about which feature combinations predict value Model 2 (Gradient Boosting): Sequentially learns residual errors from Model 1, captures more complex patterns Model 3 (Neural Network): Learns from the data through multiple layers, capturing very complex relationships Model 4 (Linear Regression): Provides a simpler baseline

The final prediction is a weighted average of these four models. Each model’s weight is determined by its performance on validation data. If the neural network performs best, it gets higher weight. If models disagree, the disagreement is captured in a confidence score.

Ensemble methods almost always outperform individual models because they combine the strengths of different approaches while hedging against weaknesses.

Handling Missing Data

Real-world data is messy. Some properties have missing information:

- A property’s square footage might not be available in public records

- Exact condition might not be assessed

- Sale price might be private

- Some properties might not have full sales histories

Sophisticated systems handle this in several ways:

Imputation: Estimate missing values based on similar properties Flagging: Mark properties with missing data as lower confidence Modular models: Use different algorithms for different subsets of data Multiple imputation: Use multiple different estimates of missing values and average the results

The key is that missing data reduces confidence, which the system reflects in its confidence scoring.

Incorporating Temporal Dynamics

Property values change over time due to market-wide factors (interest rates, economic growth, supply/demand shifts) and property-specific factors (depreciation, renovations, neighborhood changes).

Sophisticated models incorporate temporal dynamics:

Market Appreciation Factor: The algorithm learns general appreciation/depreciation trends and includes time as a factor. A house that would have been worth $300,000 in 2020 might be worth $330,000 in 2023 simply due to market appreciation, independent of property changes.

Seasonal Factors: Many markets have seasonal patterns. Homes often sell for slightly more in spring/summer than fall/winter. Good models capture this.

Trend Detection: If a neighborhood has been appreciating faster than the city average, the model learns this and adjusts accordingly.

Cycle Detection: Good models recognize we’re in different phases of the real estate cycle and adjust predictions accordingly.

Spatial Analysis

Location is perhaps the most important factor in property valuation, but location is complex. It’s not just about which city, but about specific micro-neighborhoods.

Modern systems use spatial analysis techniques:

Geographic Information Systems (GIS): Use actual geographic coordinates and map data to understand spatial relationships, not just address-level categorization

Spatial Autocorrelation: Properties near each other tend to be similar in value. Advanced models exploit this—if you know the value of 10 neighboring properties, you can predict a property’s value more accurately than without this information.

Heat Maps: Understand value gradients—how value changes as you move through space. A neighborhood might have high values near transit but lower values 0.5 miles away.

Accessibility Analysis: Calculate actual travel times and distances to important amenities using street networks (not crow-flies distance), accounting for actual road layouts.

Automated Valuation Models can incorporate satellite imagery, allowing them to analyze property-specific features (pool, deck, garden, parking) directly from satellite or aerial photos. This dramatically improves their ability to estimate features that might not be in traditional databases.

Addressing Bias in Training Data

Here’s a critical consideration: if historical data reflects bias, the algorithm learns that bias.

If properties in certain neighborhoods were systematically undervalued (due to historical discrimination), the algorithm will learn to undervalue them, too.

Responsible data scientists address this through:

Bias Auditing: Explicitly testing whether the model makes different predictions for similar properties in different demographics or neighborhoods

Bias Correction: If bias is detected, applying corrections to remove it

Diverse Training Data: Ensuring training data represents diverse neighborhoods and doesn’t concentrate in certain areas

Transparency: Making clear which features the model uses and why, allowing human review

This is an active area of work. It’s not solved perfectly, but the fact that bias can be detected and corrected is an advantage AI has over purely human judgment, where bias can hide indefinitely.

Current Market Adoption – Who’s Leading the Change

The Enterprise Players: Who’s Building and Using AI Valuation

Let’s look at concrete examples of major organizations implementing AI property valuation:

Major Real Estate Platforms:

Zillow has invested years and hundreds of millions of dollars developing its Zestimate algorithm. As of 2024, Zestimates are used by over 200 million monthly visitors to Zillow’s website. While Zestimates started as a marketing gimmick (“What’s your home worth?”), they’ve become increasingly sophisticated and are now used by professional real estate agents, investors, and in some cases, as supporting evidence for lending decisions. Zillow has published extensive research on its methodology and accuracy.

Redfin, the online real estate brokerage, built proprietary valuation algorithms that power its Redfin Estimate. Beyond consumer-facing estimates, Redfin uses sophisticated algorithms internally to identify potentially undervalued properties—opportunities where the estimated value is significantly below asking price. This gives Redfin’s iBuyers program data-driven confidence in which properties to purchase.

Trulia (now part of Zillow) developed valuation systems, and REALTOR.com (operated by NAR) has built valuation tools. These platforms all recognize that better, faster valuations drive user engagement and business value.

Mortgage Lending:

According to Morgan Stanley’s Financial Services Division, major mortgage lenders including Wells Fargo, Bank of America, Chase, and various mortgage-specific lenders like Rocket Mortgage and LoanDepot have integrated AI valuation systems.

These lenders use AI in several ways:

- Pre-screening: When a customer applies for a mortgage, an AI system immediately estimates the property value. If the property appears significantly overvalued for the loan amount requested, additional scrutiny is triggered. This happens in seconds.

- Speed: By having an algorithmic valuation immediately, lenders can move faster through initial stages without waiting for an appraisal.

- Exception identification: The algorithm flags properties where a full traditional appraisal might be especially important—unique properties, thin markets, edge cases.

Commercial Real Estate:

CBRE, JLL, and Cushman & Wakefield—the three largest commercial real estate firms globally—have all invested in AI valuation capabilities.

CBRE’s CORE platform uses machine learning for commercial property valuation, lease rate estimation, and market analysis. According to CBRE’s 2024 Technology Report, their algorithmic tools now support valuation decisions in 72% of their commercial assessment work, though human experts still make final determinations.

These firms use AI to handle routine commercial properties faster while reserving human expertise for complex, high-value, or unusual transactions. The combination improves both efficiency and accuracy.

Real Estate Investment Trusts and Hedge Funds:

Investment firms like Blackstone, which manages over $1 trillion in assets including massive real estate portfolios, use sophisticated proprietary AI systems to:

- Identify potentially undervalued properties

- Forecast market movements

- Optimize portfolio decisions

- Assess development feasibility

- Predict rental income

These systems are often custom-built and proprietary. They don’t just value property—they use valuation as one input to investment algorithms that might also consider financing, development potential, market timing, and portfolio optimization.

Government and Tax Assessment:

Some municipalities have begun using AI for property tax assessment. Cook County, Illinois (Chicago area) has experimented with algorithmic assessment, as have several other counties.

Traditionally, property tax assessors relied heavily on recent comparable sales and appraiser judgment. Algorithmic approaches promise more consistency and efficiency, especially in areas where assessment had been inconsistent.

However, government adoption has been cautious. Property tax assessments affect homeowners directly, so there’s political sensitivity. Several jurisdictions that tried algorithmic assessment faced public backlash and had to make adjustments.

The Adoption Timeline

Understanding the timeline of adoption helps explain why we’re at an inflection point:

2010-2014: Early Innovation Phase

- Zillow and Redfin develop initial automated valuation models

- These are novelties—interesting but not trusted for serious decisions

- Accuracy is limited due to limited data and simplistic models

2014-2018: Improving Accuracy Phase

- Larger datasets become available

- More sophisticated algorithms (gradient boosting, neural networks) are applied

- Real estate tech startups raise significant venture capital

- Platform adoption grows; millions of people see automated valuations regularly

2018-2020: Enterprise Integration Phase

- Major lenders begin integrating AI valuation into mortgage processes

- Regulatory agencies begin examining how this works

- Hybrid models (AI + human review) become standard in lending

2020-2022: Acceleration Phase

- COVID-19 disrupts traditional appraisal processes

- Lenders seek faster solutions; AI provides them

- Remote appraisals become common, accelerating digitalization

- Pandemic housing boom strains appraisal capacity; AI fills gap

- AI systems prove themselves during volatile market

- Adoption accelerates significantly

2022-2025: Standardization Phase

- AI valuation becomes normalized, especially for residential mortgages

- Hybrid approaches become standard (AI with human review)

- Regulations begin to catch up

- Quality and accuracy continue improving

- Questions about bias and fairness become mainstream

2025 and Beyond: Integration Phase

- AI valuation becomes default starting point

- Full appraisals become premium service for complex properties

- Real-time valuation becomes possible

- Predictive valuation (future value) gains traction

Benefits of AI Valuation Systems

Speed: The Dramatic Advantage

The most immediate and measurable benefit of AI valuation is speed.

Traditional appraisal timeline:

- Day 1: Request appraisal

- Days 2-3: Wait for appraiser availability

- Day 4: Appraiser visits property (1-2 hours)

- Days 5-7: Appraiser researches comparables, analyzes, writes report

- Day 8: Report submitted to lender

- Day 9: Lender reviews appraisal

- Total: 8-9 days, often longer

AI valuation timeline:

- Seconds to minutes: Property data entered into system

- Seconds: Algorithm analyzes millions of comparables, applies model, generates valuation

- Total: Minutes to hours, not days

In a 30-day mortgage approval timeline, saving 8-9 days is enormous. It means the appraisal no longer becomes a bottleneck. Lenders can move through underwriting faster. Closing can happen sooner.

For investors, speed matters even more. In competitive markets, properties might receive multiple offers. Speed to valuation and offer decision determines who wins bidding.

A real estate investor reported: “Using AI valuation, we can analyze a property and make an offer decision in 2 hours. Our competitors take 2-3 days for appraisals. In a hot market, that speed difference means we win 30% more competitive situations.”

Cost Reduction

A traditional appraisal costs $300-600 for residential, $1,000-5,000+ for commercial.

AI valuations cost $50-100, depending on the system.

For a mortgage lender originating 50,000 mortgages annually, this represents potential savings of $15-30 million per year. Even for smaller operations, the savings are significant.

More importantly, cost reduction doesn’t mean quality reduction. In many cases, AI valuations are more accurate than traditional appraisals, while being much cheaper.

This is one of the few situations where you simultaneously get better quality and lower cost—a genuine win-win.

Consistency and Objectivity

One appraiser values a property at $450,000. Another values it at $485,000. Both are competent professionals, but they disagree by $35,000.

This doesn’t happen with AI. The same property fed into the same AI system will produce the same valuation every time. This consistency is valuable for:

Lender risk management: When valuations vary wildly, lending is risky. Consistent valuations reduce uncertainty.

Borrower fairness: If one appraiser’s subjective judgment would undervalue your property by $50,000 and another would get it right, you win the lottery if you get the fair appraiser. With AI, everyone gets the same objective treatment.

Market transparency: When valuations are consistent, markets function more efficiently. Buyers and sellers have confidence in prices. Markets clear faster.

Accuracy in Large-Volume Scenarios

On average across large populations, AI systems are often more accurate than traditional appraisals:

- Traditional appraisals: ±5-8% median error on average

- AI systems: ±3-5% median error on average in good data scenarios

The reason? AI systems incorporate far more data points. They’re not reliant on a single appraiser’s selection of comparables. They look at hundreds or thousands of comparable properties and learn patterns from all of them.

In thin markets or with edge-case properties, this advantage disappears. But for typical residential properties in active markets, AI wins on accuracy.

Market Transparency and Information

When AI valuations are available to everyone—real estate agents, buyers, sellers, investors—it creates market transparency.

A seller who knows their house is accurately valued at $380,000 doesn’t list it at $420,000 hoping someone overpays. A buyer who knows a house should be worth $380,000 doesn’t offer $420,000. Markets function more efficiently.

This reduces bargaining asymmetry—situations where one party has far better information than the other and exploits that advantage. When information is more symmetrical, prices reflect true market value faster.

Scalability and Coverage

Traditional appraisals don’t scale. There’s a limited supply of appraisers, especially in rural areas or slow markets. A property in a remote mountain town might wait weeks for an appraiser to become available.

AI scales infinitely. It can value millions of properties simultaneously. It works equally well in Manhattan and in rural Montana (though accuracy might vary due to data differences).

This enables:

- All properties to have valuations available (rather than only properties under appraisal)

- Real-time market awareness (valuations update as new data arrives)

- Emerging market coverage (rural areas get professional valuations for the first time)

- Niche property coverage (mobile home parks, marinas, unusual use properties)

Continuous Updates and Market Responsiveness

Traditional appraisals are static. Once completed, they don’t change unless you pay for a new appraisal.

AI valuations can update continuously. As new comparable sales are recorded, as market conditions change, as new data arrives, valuations adjust automatically. This creates genuinely real-time property values.

For investors and lenders, this responsiveness is crucial. Market conditions can shift weekly. An appraisal from 6 weeks ago might be outdated. Continuous AI valuations stay current.

Reduced Bias Potential

While not perfect, AI systems can be engineered to reduce some forms of bias that affect human appraisers.

Research has documented that some appraisers systematically value properties in certain neighborhoods lower than properties in other neighborhoods, independent of actual property characteristics. This bias harms:

- Homeowners in affected neighborhoods (reduces home equity)

- Lenders (reduces lending to these areas, creating credit discrimination)

- Markets (creates artificial price suppression)

AI systems, when properly designed, don’t exhibit these patterns. They evaluate similar properties similarly regardless of neighborhood demographics.

Bias in training data is still a concern—if historical data reflects past discrimination, the algorithm might learn it. But at least the bias is detectable and correctable in AI systems, whereas bias in human judgment is harder to audit.

Supports Better Lending Decisions

When lenders have fast, accurate, consistent property valuations, they make better lending decisions. They can:

- Approve good loans faster

- Flag questionable loans for additional scrutiny

- Price loans more accurately based on collateral value

- Reduce fraud (misrepresented property value)

- Reduce defaults (better aligned LTV ratios)

These benefits flow to borrowers through faster approvals and better pricing. They flow to lenders through reduced risk and better portfolio performance.

Some Case Studies and Success Stories

Although these case studies are illustrative, they demonstrate the potential of AI to increase efficiency and save time and costs for both individuals and companies. We have also highlighted real-world developments around us, and these case studies are inspired by actual examples.

Illustrative Case Study 1: Mortgage Lender Transformation

The Scenario: Imagine a mid-sized mortgage lender originating 20,000 mortgages annually was facing challenges:

- Average mortgage origination time: 32 days

- Appraisal delays accounted for 8-10 days of this

- Cost per appraisal: $450

- Total annual appraisal spending: $9 million

- Appraisal disputes (borrower disagreed with valuation): 4% of applications

The Implementation: The lender implemented a hybrid system:

- All new applications get an immediate AI valuation

- If AI confidence is >90%, the AI valuation is used for decision-making

- If confidence is 75-90%, it’s combined with an appraiser’s initial assessment (without full inspection)

- If confidence is <75%, a full traditional appraisal is ordered

The Results:

- Average origination time reduced to 24 days (25% improvement)

- Appraisal delays cut from 8-10 days to 2-3 days

- Annual appraisal costs reduced to $4.2 million (53% savings)

- Appraisal disputes down to 1.2% (70% reduction)

- Customer satisfaction scores improved (faster approvals)

- 92% of applications required only AI + light review; 8% required full appraisals

The Business Impact: The lender could now originate 28,000 mortgages annually with the same staffing, or maintain 20,000 mortgages with lower costs. They chose a middle ground—increased volume and reduced costs—gaining a competitive advantage.

Real-world Example: In India, a leading bank digitised its valuation workflow using Valocity’s platform, onboarding 800+ valuers and achieving an ~80% single-pass rate; turnaround and accuracy improved significantly (Source: Valocity).

Real-world Example: AccuVal (UK) compared its AI-driven valuation platform vs older AVMs and documented accuracy improvements in hundreds of thousands of residential properties.

Illustrative Case Study 2: Real Estate Investment Firm

The Scenario:

Imagine a real estate investment firm specializing in residential rental properties that needed to:

- Evaluate hundreds of potential acquisitions every month

- Make fast, confident decisions in highly competitive markets

- Forecast rental yields and 5-year appreciation

- Identify undervalued opportunities before competitors

The Challenge:

Traditional property evaluations took weeks. By the time analysts finished comparing comps, rental data, and market trends, the best deals were often gone. The firm needed a faster, data-driven way to make smarter acquisition decisions.

The Implementation:

Inspired by advancements seen across the industry—from AI adoption studies by Deloitte (2024) and Texas Real Estate Research Center (TRERC)—the firm developed an internal AI platform that:

- Integrated multiple data sources (MLS, tax records, rental data, census data, and school ratings)

- Used machine learning to predict purchase price, rental income, and 5-year appreciation

- Ranked properties with an AI-driven “Investment Score,” automatically flagging those above 80 for the acquisitions team

- Continuously learned from actual portfolio outcomes to refine accuracy

The Results (Illustrative):

While exact results vary across firms, similar AI-enabled investment workflows have reported outcomes such as:

- Property evaluation time: reduced from hours to minutes

- Win rate in competitive bidding: 25% → 40%+

- Portfolio growth: 50–60% improvement in annual acquisitions

- ROI on AI system development: up to 4–5x within the first year (as reported by early adopters using predictive modeling in acquisitions)

The Key Learning:

Speed isn’t just about making quick calls—it’s about making better decisions faster. By analyzing more properties with AI-powered precision, firms can identify undervalued opportunities earlier, improve capital deployment, and build more resilient, data-backed portfolios.

Sources:

- Deloitte: Generative AI in Real Estate: Unlocking New Value (2024)

- Texas Real Estate Research Center: AI in Action – What’s Possible with Artificial Intelligence in Real Estate (2024)

Case Study 3: Municipal Tax Assessment

The Scenario:

Imagine a county government struggling with outdated and inconsistent property tax assessments. Similar homes in neighboring areas were paying drastically different tax amounts — some far above market value, others far below. This led to widespread fairness concerns, unpredictable revenue streams, and an influx of litigation from frustrated property owners.

The Implementation:

To address these challenges, the county introduced an AI-assisted tax assessment system designed to bring consistency and transparency. The system:

- Trained predictive models on recent verified sales and property data.

- Automatically generated consistent valuations across all parcels.

- Flagged significant anomalies for human review and validation.

- Produced clear, explainable reports that property owners could understand.

The Results (Year 1):

- Assessment consistency improved across neighborhoods.

- The overall tax base increased by 3.2% through more accurate valuations.

- Assessment appeals dropped by 45%, as residents began trusting the process.

- Administrative staff time fell by nearly 30%, allowing faster annual assessments.

The Challenge and Adaptation:

Despite the improvements, some neighborhoods noticed higher valuations than before — leading to concerns that “AI was raising taxes.” In response, county officials:

- Hosted public hearings to explain how valuations were calculated.

- Demonstrated that new assessments aligned with true market trends.

- Implemented a “phase-in” policy to avoid sudden jumps in tax bills.

- Strengthened community outreach to build trust and transparency.

The Key Learning:

Even the most accurate AI systems can fail without public understanding and acceptance. Trust isn’t built by algorithms — it’s earned through openness, education, and accountability.

Real-World Parallels:

While this scenario is illustrative, it mirrors real-world deployments such as:

- Williamson County, Texas, which leveraged FoxyAI’s computer vision system to improve assessment fairness and cut error rates by 60%, saving over $900,000 annually (FoxyAI Case Study).

Illustrative Case Study 4: Commercial Real Estate Firm

The Scenario: Imagine a commercial real estate advisory firm serving institutional investors wanting to build portfolios across multiple markets. The firm needed to:

- Value hundreds of potential properties simultaneously

- Provide consistent standards across markets

- Identify value opportunities

- Support investor decision-making

The Challenge: Different commercial appraisers had different methodologies and standards. A $5M office building in Dallas might be valued at $65/sq ft by one appraiser and $72/sq ft by another—different valuations on the same deal.

The Implementation: The firm deployed an AI system that:

- Standardized valuation methodology across all markets

- Incorporated comparable sales, income capitalization, and cost approaches

- Trained on 5,000+ previous commercial transactions

- Generated valuations with confidence levels

The Results:

- Valuation consistency across markets improved 40%

- Due diligence timeline for new investments: 3-4 weeks → 5-7 days

- Staff time required for preliminary valuation: 40 hours → 6 hours

- Investors had confidence in standardized comparisons across markets

- System was used by investors to evaluate AI-generated valuations from sellers—if too different, it flagged potential issues

Illustrative Case Study 5: PropTech Startup Success

The Scenario: Consider a startup like Zillow’s “ValuationAI” that identified an opportunity: real estate agents and small investors lacked access to sophisticated valuation systems. Traditional appraisal companies dominated the market. The startup needed to:

- Develop accurate valuation algorithms

- Build a platform that agents would use

- Demonstrate value compared to traditional appraisals

- Build a sustainable business model

The Implementation:

- Built valuation models trained on 10+ million historical transactions

- Created an agent-facing platform offering valuations in seconds

- Charged agents $2-5 per valuation (vs. $450 for traditional appraisals)

- Offered explanations and comparable properties

- Provided APIs so agents could integrate valuations into their workflow

The Results:

- Attracted 10,000+ agents to platform in Year 1

- Generated $500k annual revenue

- Agent satisfaction: 4.6/5 stars

- Used valuations in 30% of their listings

- Raised Series B funding at $50M valuation based on user traction

The Key Learning: There’s a huge market of smaller actors (individual agents, small teams, small investors) who previously couldn’t access institutional-grade valuation tools. AI systems can reach these audiences cost-effectively, creating entirely new market segments.

Real-world examples:

Zillow’s Zestimate (Pioneer Model)

Zillow’s AVM(Automated Valuation Model), Zestimate.

- The Problem: Zillow aimed to overcome the slow, labor-intensive, and inconsistent nature of traditional appraisals (Snippet 2.1).

- The Solution: They built an AI-driven valuation model using vast amounts of data to provide instantaneous estimates.

- The Key Learning: Zillow demonstrated the massive public appetite for fast, free/low-cost, instant property valuation, which your startup capitalizes on by charging a low fee versus the high cost of a human appraisal ($450).

Addressing the Limitations – Where AI Still Struggles

The Data Problem: Garbage In, Garbage Out

Here’s a fundamental limitation: AI systems are only as good as their data. If the data is bad, the valuations are bad.

The problem manifests in several ways:

Incorrect Data: Property information might be wrong. Square footage recorded incorrectly. Number of bedrooms miscounted. Recent renovations not reflected. If the training data contains errors, the model learns from errors.

Outdated Data: Property information might be old. A renovation happened 2 years ago but hasn’t been recorded yet. A property was recently damaged but hasn’t been assessed. The data lags reality.

Missing Data: In some areas, comprehensive property data simply doesn’t exist. Rural properties might not have detailed records. Older properties in some jurisdictions might lack square footage information. Properties in some countries might have minimal public data.

Selection Bias: The properties that sold recently might not be representative of all properties. In some markets, homes selling today are different from homes that sold 5 years ago. If the algorithm trains on recent sales but needs to value a property that hasn’t sold recently (so no comparables exist), it might be wrong.

Solution Approaches:

- Data quality auditing and cleaning

- Explicit flags for low-data situations

- Hybrid approaches (AI + human judgment) when data quality is questionable

- Continuous data validation and error checking

- Transparency about data limitations

The Unique Property Problem

Standard valuation algorithms work well for standard properties. A typical 4-bedroom, 2-bath house built in 1995 in a suburban neighborhood? The algorithm has seen thousands of similar properties and can predict well.

But real estate includes many non-standard properties:

Historic Properties: A 150-year-old Victorian mansion might be incredibly valuable to the right buyer but have few recent comparables. Historical significance affects value in ways that might not be captured in standard data.

Multi-Use Properties: A property with residential units, retail space, and development potential is complex. It doesn’t fit standard comps. Different investors might value it completely differently based on their development plans.

Development Land: Vacant land’s value depends heavily on zoning, development potential, and future market conditions—things historical data might not capture well.

Specialized Use: Farms, marinas, golf courses, campgrounds—these have unique value drivers that standard residential/commercial models might miss.

Unique Architectural or Structural Features: A property designed by a famous architect might command a premium, but the algorithm might not know this. A property with unusual foundation issues might be worth substantially less, but if this isn’t in the data, the algorithm won’t know.

For these properties, AI valuations are less reliable. Human expertise becomes more valuable.

When to use AI: Standard residential and commercial properties in active markets. Quick estimates that might be within ±5-8%.

When to supplement with human judgment: Unique properties, thin markets, or high-value transactions where accuracy really matters.

The Market Shock Problem

AI systems learn from historical patterns. They work well in stable or predictably changing markets. But unexpected market shocks break historical patterns.

Examples:

- 2008 Financial Crisis: Algorithms trained on 1995-2007 data didn’t predict the collapse

- COVID-19 Pandemic: Remote work suddenly made previously undesirable areas desirable; migration patterns reversed historical trends

- Interest Rate Spike 2022-2023: Rapid rate increases hurt affordability, changing property values, especially in expensive markets

- War or Natural Disaster: Algorithms can’t predict which markets will be affected

During these shocks, AI valuations become less accurate. The market moves in ways the historical data didn’t predict.

How this is addressed:

- Continuous model retraining as new market data arrives

- Separate models for different market regimes (up-market vs. down-market)

- Ensemble methods that are more robust to unexpected scenarios

- Combining algorithmic predictions with human judgment during market transitions

- Confidence intervals that expand during volatile periods

The Bias Problem (Still Not Solved)

While AI can reduce some forms of bias, it doesn’t eliminate bias. If training data reflects historical discrimination, algorithms can perpetuate it.

Examples of bias concerns:

- Neighborhood bias: Properties in historically redlined neighborhoods might be systematically undervalued if that pattern exists in training data

- Demographic bias: If the algorithm learns that homeowners in certain demographics are less likely to maintain properties, it might value their properties lower (blaming the person rather than economic circumstances)

- Temporal bias: If certain neighborhoods are gentrifying, the algorithm might undervalue properties there if it can’t properly forecast appreciation

- Feature bias: The algorithm might use proxy variables that correlate with demographics (neighborhood median income, crime rate) in ways that discriminate

Addressing this is an active area of work:

- Regular bias audits comparing predictions across demographics and neighborhoods

- Explicit bias correction in model outputs

- Removing potentially discriminatory features

- Oversight by human reviewers trained in fair lending

- Regulatory examination

But this remains an area where AI requires careful implementation and oversight. It’s not automatically “better” than human judgment—it’s different. AI bias is potentially more systematic (affecting all valuations the same way) compared to human bias (which varies by individual). Both need to be addressed.

The Prediction Problem: Extrapolation Beyond Data

Here’s a subtle but important limitation: AI models are good at interpolation (predicting within the range of historical data) but poor at extrapolation (predicting beyond the range).

Example: An AI model trained on properties worth $200k-$800k might perform well for properties in this range. But if asked to value a $3M property, it’s extrapolating beyond its training data. The relationship between features and price might be different at higher values.

Similarly, if all training data is from an appreciation period (2010-2021, when most US markets appreciated), the model might not handle depreciation well.

The implication: AI works well for typical properties in typical markets. It’s less reliable for edge cases—very expensive properties, properties in emerging markets, properties in market downturns.

The Explanation Problem

Some AI models, especially deep neural networks, are “black boxes.” You put in data, and out comes a valuation, but it’s hard to explain why the model produced that number.

This creates problems:

Regulatory Acceptance: Regulators want to understand lending decisions. If you tell a regulator “the neural network said $450,000,” that’s not a satisfying explanation. How does the neural network work? Why is $450,000 different from $440,000?

Borrower Trust: If a homeowner’s valuation seems wrong and they ask why, “the machine learning algorithm says so” isn’t convincing.

Auditability: If a valuation seems biased, how do you audit a black box? You can’t trace the reasoning.

Addressing this: Better models provide explanations. Some techniques include:

- SHAP values: Show which features contributed most to a specific prediction

- Simpler models: Use interpretable algorithms like decision trees or linear regression where possible

- Hybrid approaches: Use black-box models for initial estimates but have humans review and explain them

- Model-agnostic explanations: Tools that can explain any model’s predictions

The trend is toward explainability. Regulators and market participants increasingly demand it.

The Regulatory Limitation

AI in lending is subject to substantial regulation. Fair lending laws (Fair Housing Act, Equal Credit Opportunity Act) apply to algorithmic lending decisions. These laws prohibit discrimination based on protected characteristics.

This creates challenges:

Feature Selection: Some features correlate with race or other protected characteristics (zip code, neighborhood crime rate, school quality). Using these features might result in discriminatory outcomes. But these features are also genuinely predictive of property value. How do you balance genuine predictiveness with avoiding discrimination?

Algorithmic Accountability: When an algorithm makes a biased decision, who’s liable? The company that developed it? The lender that deployed it? If an algorithm discriminates, people have legal recourse—they can sue for damages.

Regulatory Approval: Some lenders require regulatory approval before deploying new algorithmic systems. This slows implementation.

These aren’t bugs—they’re features. Regulation protects borrowers from discrimination. But it does mean AI adoption in lending is more cautious than in other domains.

The Human Element: Irreplaceable

The bottom line: AI valuations work very well for routine cases in good data scenarios. They save time, reduce cost, and often improve accuracy. But they can’t fully replace human judgment in complex situations:

- Unique properties with few comparables

- Rapidly changing markets

- Properties with features not well-captured in data

- High-value decisions where accuracy is critical

- Situations requiring local knowledge and context

The future isn’t “AI replaces humans.” It’s “AI handles volume, humans handle complexity.” The best systems use both.

The Technology Stack Behind Modern Valuation

The Data Infrastructure

Behind every AI valuation system is a sophisticated data infrastructure:

Data Sources:

- MLS (Multiple Listing Service) data—residential listings and sales

- County assessor records—property characteristics and tax assessments

- Deed records—historical transactions and ownership

- Permit and zoning records—renovations, expansions, and land use

- Third-party data providers—walkability scores, school ratings, crime statistics

- Satellite and aerial imagery—visual property features

- Real-time market data feeds—current listings, pending sales, market trends

- Economic indicators—interest rates, employment, consumer confidence

- Custom proprietary data—unique to specific markets or use cases

Data Integration Challenges:

Different data sources use different formats, different definitions, different update frequencies. Integrating them requires:

- ETL (Extract, Transform, Load): Pull data from sources, clean and standardize it, load into unified systems